The GENIUS Act's passage and the incorporation of onchain stablecoins have created a framework that necessitates the development of onchain capital markets to maximize their potential. Stablecoins support payments, remittances, and DeFi yield generation, offering annualized yields of 4%-10.3% in real-world asset DeFi (and higher rates in crypto asset DeFi) versus 0.46% average savings account yields in banks. This difference will enhance deposit migration among tech-savvy users to DeFi. Meanwhile, businesses who currently bear up to 3% interchange fees for electronic credit card payments will drive adoption of stablecoins for payment purposes. These economic realities will accelerate deposit migration onchain among tech-savvy users, where stablecoins should be channeled to economically productive uses.

Without prudent oversight, this shift risks financial instability, regulatory gaps, and unequal access to opportunities. The Treasury can mitigate these risks by fostering onchain capital markets that prioritize SME lending, a critical driver of US economic growth.

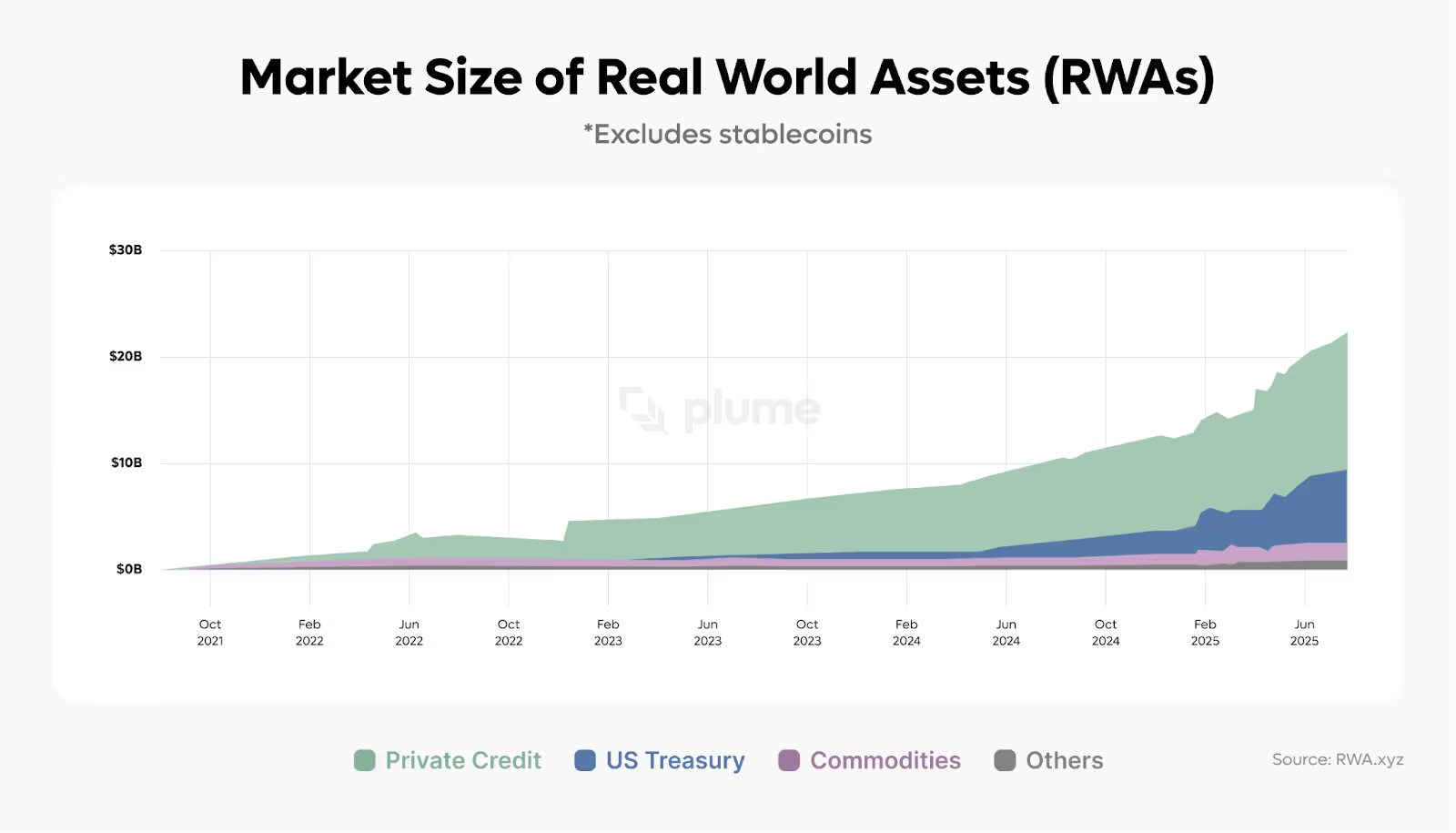

Plume Network Inc. (Plume) is already seeing an interest in yield from global users for US SME yields embedded in permissionless tokenized real-world assets (RWA) providing returns that can exceed 10%. According to RWA.xyz, since January private credit tokenized RWAs (which often include bundles of SME loans) have grown from less than $10 billion to over $13 billion in the first six (6) months of 2025. We can expect this trend to accelerate as US consumers and businesses migrate to onchain environments.

The transition to onchain capital markets propelled by the GENIUS Act is driven by economic incentives that align yield opportunities with capital flows, facilitated by low search and transaction costs. Tokenization and community bank origination amplify these incentives, attracting stablecoin capital to SME lending.

Capital flows efficiently when search costs (finding viable borrowers) and transaction costs (intermediation, settlement) are low. Transaction cost economics, per Coase and Williamson, posits that markets thrive by minimizing these frictions. In traditional SME lending, high search costs create a niche for community banks. “Community banks tend to focus on loans as relationships, originating loans that require local knowledge, a greater personal touch, individual analysis, and continued administration rather than loans that can be made according to a formula.” (Quoting a 2020 FDIC study).

Onchain finance preserves community banks' advantage in search costs for SME lending, but tokenization reduces transaction costs, enabling distribution of SME loans in blockchain environments. To support this under the GENIUS Act, the SEC must create rules encouraging onchain capital formation, while banking and SEC regulations govern DeFi to offer safe tokenized yield. In particular, blockchain technology reduces the cost of securitizing SME loans. According to Deloitte, blockchain technology and tokenization can streamline processes (automate manual tasks), enable real-time data sharing (minimizing delays and errors), reduce administrative costs, enhance security, and enable faster transactions.

Community banks and tokenized SME lending

Community banks, with their local expertise, reduce search costs by identifying creditworthy SMEs, while onchain technology enables them to distribute loans into blockchain environments compliant with the GENIUS Act. This creates a new opportunity for community banks to shift from a lending to an origination model for SME loans, channeling stablecoins productively The increased availability of SME loans and lower transaction costs will likely lead to “greater efficiency of loan origination” as the IMF observed investigating the rise of securitization of mortgages. For stablecoins to succeed without offering yield, this path requires banking and SEC rules for DeFi to ensure safe tokenized opportunities.

Plume’s role in bringing capital markets onchain

At the core of our “Plumerica” initiative, we are working with the SEC to bring parts of the Plume ecosystem into America under a regulatory framework tailored for onchain capital markets. Despite restrictioning US users from entry portals controlled by Plume Network Inc. nevertheless, we, alongside other US-based blockchain developers (many with similar restrictions) are seeing growing demand for US dollar capital markets assets onchain. In just eight (8) months since October 2024, the non-stablecoin RWA markets have more than doubled to over $23 billion.

Operational efficiency and enhanced onchain distribution drives issuer interest, while low-risk (Treasuries) or high yield (private credit) are driving investor demand.

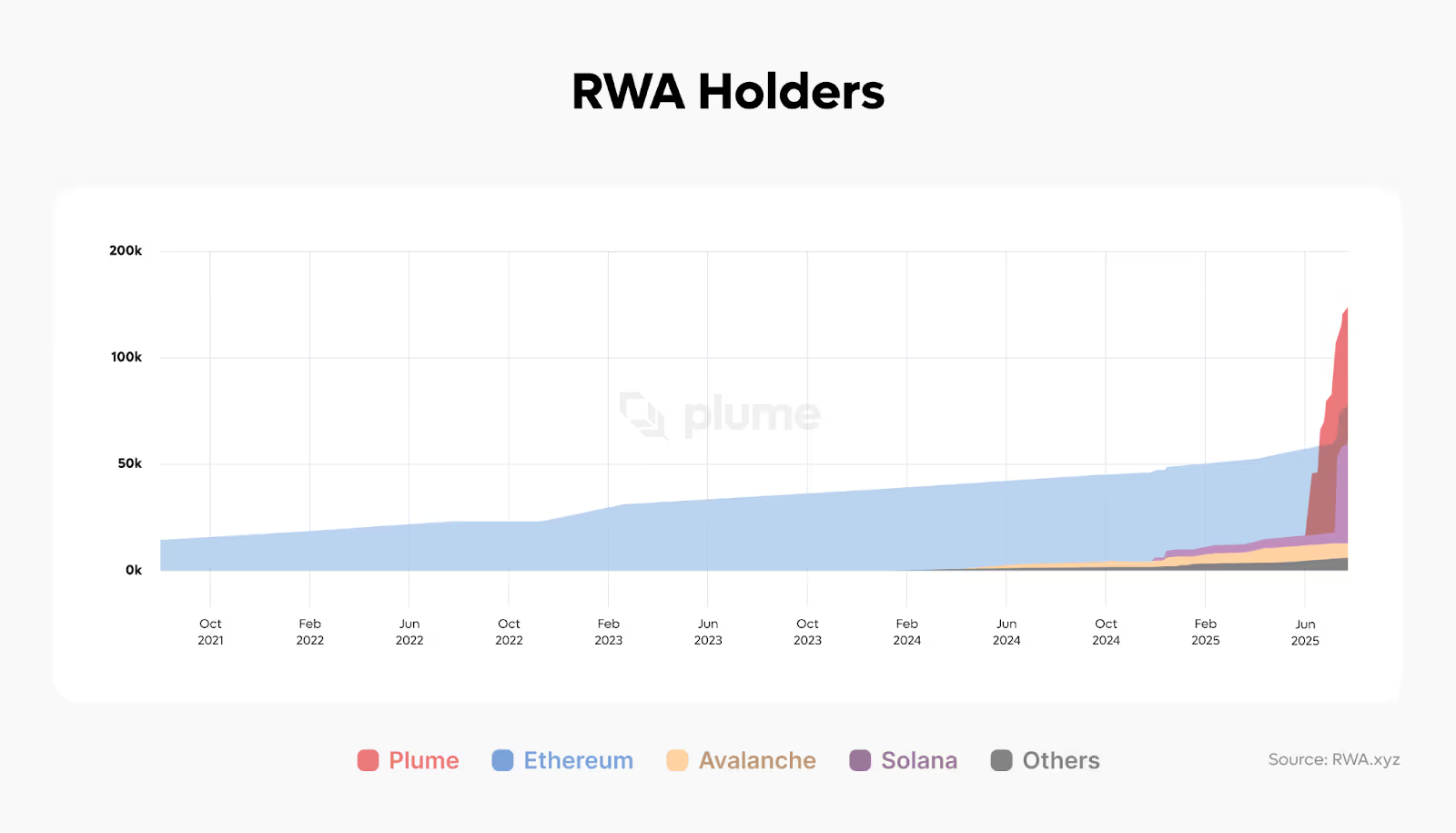

Plume is driving much of this growth. Since launching our mainnet in May, the Plume Network has eclipsed all other blockchain networks by number of wallet addresses with tokenized RWA assets. In the 30 days ending July 17, 2025, Plume total value locked (TVL) has grown 80% with over $150 million.

Policy recommendations

GENIUS policy is now a reality as it relates to stablecoins. While a core goal of the GENIUS Act is to enhance access to US dollars by leveraging low-cost global distribution provided by open blockchains, the goal of capital markets policy should be to enhance access to capital markets leveraging the same open blockchain rails. Toward this goal, we recommend the following (all lower-case) genius capital markets policy initiatives as a part of a comprehensive package:

- Promoting regulatory clarity at SEC

- Clarification regarding the tokenization of offchain securities. Currently, there is a “race to the bottom” as US-based blockchain innovators sidestep US markets to provide foreign investors access to the US and US dollar-denominated assets they want. The SEC should create clear pathways to encourage tokenization of securities and their distribution onto open, public blockchains through a comprehensive review of its rules and regulations. We recommend specifically two principles as the SEC undertakes this work:

- Rules tailored for the onchain environment should aim for the same or better outcomes as those driving legacy rules. This will require a close examination of the statutory authority and purpose behind existing rules and a thorough understanding of the capabilities of blockchain-based markets. We provide some specific examples following from this principle in our May 2025 comment letter to the SEC Commissioner Peirce and the Crypto Task Force.

- US issuers and registrants that comply with US rules should generally be able to distribute assets onto open, public blockchains in order to maximize capital formation opportunities and the influence of US capital markets and the US dollar.

- Further implementation of a DeFi “innovation exemption” with particular emphasis on encouraging tokenization of ABS and other securities, including investment products.

- Expanding the use of “shelf registrations” that make it easier to securitize debt assets, reducing the cost of capital for underlying borrowers by expanding eligibility for streamlined ABS registration, particularly if they relate to consumer finance, including microfinance, as well as SMEs.

- Driving innovation through bank policy related to blockchain innovation

- Provide guidance that enables banks to issue products into open, permissionless onchain environments through guidance on areas blocking innovation, particularly as it relates to operational risk and Bank Secrecy Act.

- Encouragement of partnerships between onchain entrepreneurs and community banks as the two begin to adapt to new opportunities.

- Promoting onchain safety across all financial regulators

- Consistent approaches to blockchain-related operating risks, including promotion of best practices relating to smart contract auditing and testing, are critical to ensure the safety of onchain capital markets.

- Encouraging community reinvestment through tax incentives

- Capital gains exemptions for yield generated from projects investing in the low and moderate income (LMI) communities currently benefiting from Community Reinvestment Act (CRA) requirements on US banks.

- Offer tax breaks for SME lending by community banks, modeled on Opportunity Zones, which have attracted over $100 billion in investments between 2018 and 2024.