.png)

Real-World Assets are becoming a lasting part of onchain finance. At Plume we want everyone to understand this new ecosystem, built with traditional assets. The RWA Academy breaks down everything you need to know, from the most basic explanations to more detailed financial concepts. Here, we explain what bonds are as an asset class.

At some point, almost every government has needed to borrow money. The same can be said for almost every major company. The question is always the same: how do you raise enormous sums of capital from thousands of investors at once, under terms everyone can agree to?

The answer is a bond.

They’ve financed wars, built railways, and funded sovereign nations. Perhaps most importantly, they’ve also kept corporations operating through steep economic downturns. Today, the total global bond market is more than $150 trillion, making debt securities larger than the global equity market.

Bonds are the bedrock of every economy in the world today. And increasingly, they’re the centerpiece of conversations about asset tokenization and onchain financial management.

Before we talk about tokenizing them, we need to better understand what makes a bond.

So, What's a Bond?

At its core, a bond is just a loan that’s specifically structured to be bought, sold, and traded.

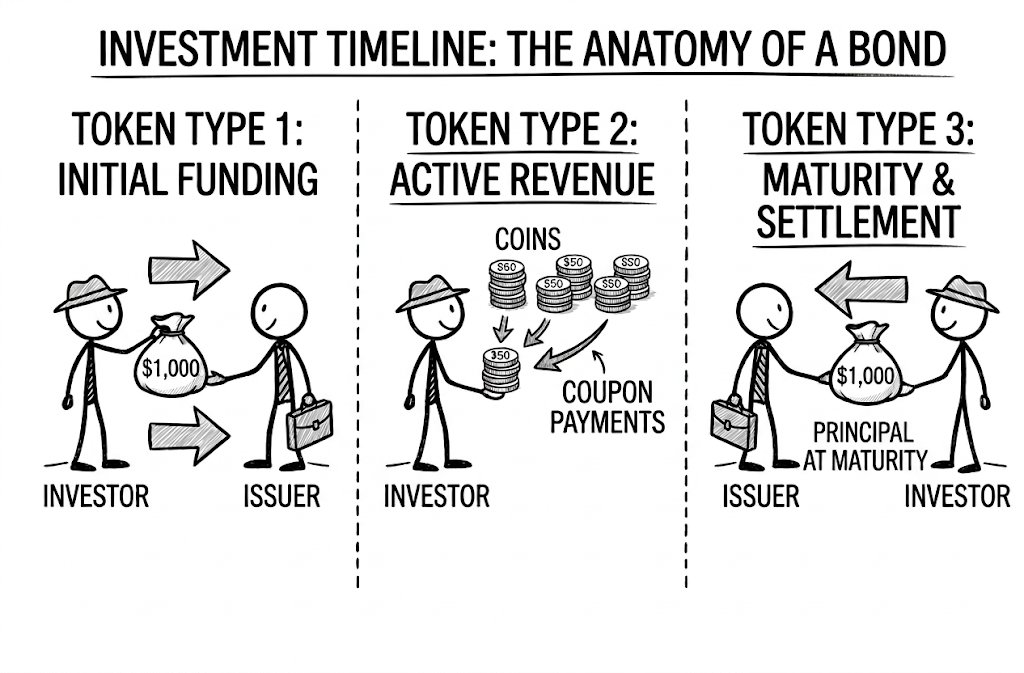

Buying a bond entails lending money to the issuer. That issuer could be a government, a corporation, or a municipality. In return, the issuer agrees to pay you interest at regular intervals and return your principal at a fixed future date.

The interest payment is called the coupon. The return date is the maturity. The amount you get back is the par value.

Unlike equity, buying a bond doesn't give you ownership in a business. You're not betting on growth. You're betting on the simple reality that you’ll be repaid what you're owed on the schedule you were promised.

Let’s use an example to get an idea of what this predictability looks like in practice. Assume you buy a $1,000 bond with a 5% annual coupon and a 5-year maturity.

That bond will return you $50 every year for five years. At the end of year five, you get your $1,000 back. Now, when it’s all said and done, you've earned $250 in interest, and your principal is completely intact. There were no surprises along the way or market volatility to contend with. The predictability was the whole point.

Why Bonds Matter in a Portfolio

Bonds generate cash flow through regular coupon payments that show up regardless of market conditions. For investors seeking consistent, scheduled returns, bonds are the most straightforward instrument available.

The contractual nature of bonds also makes them behave differently from equities. Bonds don't track sentiment or momentum. Rather, their prices are driven by interest rates, credit quality, and time. High-quality bonds generally hold their value or even appreciate during times of economic uncertainty.

Bondholders are also senior to equity holders in a company's capital structure. If a company runs into financial trouble, debt obligations are settled before shareholders see anything.

None of this means bonds are risk-free. But the nature of that risk is different, and the tradeoffs are defined from the start.

Bonds Aren’t a Single Asset Class

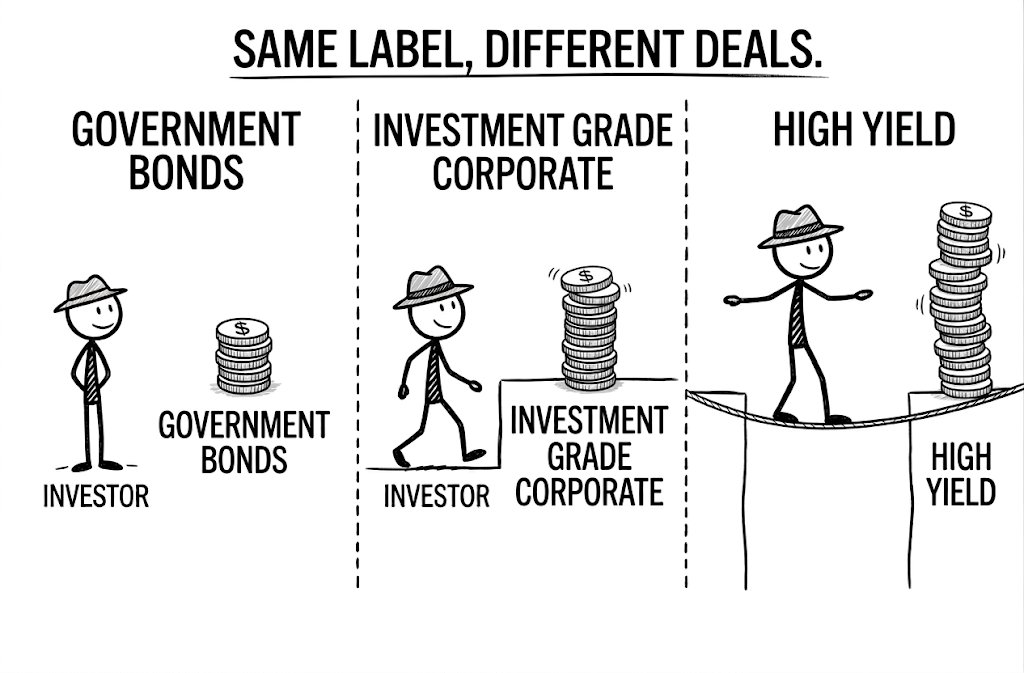

The problem with bonds is that calling something "a bond" doesn’t really tell us much. After all, a bond is just a promise to pay. In reality, bonds come in all shapes, sizes, qualities, and durations, ranging from low risk to highly speculative. Let’s take a look at some of the most common:

Government bonds are one of the most popular types of bonds. National governments issue them to finance public spending. US Treasuries are the most widely referenced example, backed by the full faith and credit of the United States.

US Treasuries are often cited as the “risk-free return,” serving as the benchmark against which virtually everything else in fixed income is priced. US treasuries are the floor, while everything else is measured by how much higher on the risk ladder you're willing to climb.

So while a bond issued by an emerging-market sovereign with unstable fiscal policy is still a government bond, it carries a completely different risk profile than a US Treasury asset.

Corporate bonds are debt issued by companies, and boasted a market size of around $41 trillion in 2025. Corporate bonds generally offer higher yields than government bonds to compensate for the additional credit risk. The differences between corporate bonds are also much more stark than those between their government bond counterparts. Apple issuing 10-year debt is a fundamentally different proposition than a leveraged buyout vehicle issuing the same instrument.

Investment-grade versus high-yield is the fundamental distinction most bond buyers consider. Financially stable entities issue investment-grade bonds with strong credit ratings. For these entities, the likelihood of default is close to zero.

Conversely, high-yield bonds carry ratings below the investment-grade threshold and offer higher returns to compensate. Naturally, the probability of default in these types of bonds is meaningfully higher. The spread between these two categories widens during economic stress and compresses during periods of confidence. Watching that spread is one of the clearest real-time indicators of how the market is pricing corporate risk, and serves as a powerful indicator for overall economic health.

Duration is perhaps the most understated yet essential variable to consider for bonds. A bond's maturity determines its sensitivity to interest rates. Generally, short-term bonds don’t react much to rate moves, while long-term bonds swing dramatically on the same news.

Nowhere is the importance of duration more evident than in 2022, when the Fed raised rates by a staggering 4 percentage points. Following the hike, the Bloomberg US Treasury Index

. Long-dated US zero-coupon bonds

, the worst performance for long-duration government debt in 200 years. A 30-year Treasury backed by the full faith and credit of the US government lost nearly 40% of its market value in a single year.

The US government’s credit was still impeccable. It’s the duration risk that delivered the damage to bondholders.

What Drives Bond Yields?

Bond yields generally reflect the interaction of three forces.

Interest rates are the dominant factor for bonds. When central banks raise rates, newly issued bonds come to market with higher coupons. Existing bonds with lower coupons become less attractive, so their prices fall, and their effective yields rise to match the market. The reverse happens when rates decline. This inverse relationship between price and yield explains why bond portfolios can lose money even when no issuer defaults and all coupons are paid on time.

Credit risk layers on top of rates. The more uncertain the market is about whether an issuer will repay, the more yield investors demand. This additional premium is the credit spread. A US Treasury and a high-yield corporate bond might both mature in ten years, but a wide spread separates their yields because they carry fundamentally different repayment risks.

Time compounds both of the above. Longer-maturity bonds generally offer higher yields to offset uncertainty about future inflation, rates, and issuer health. This relationship is captured in the yield curve. When it inverts, with short-term yields exceeding long-term yields, it has historically preceded every US recession in modern history.

Why Bring Bonds Onchain?

Tokenizing a bond doesn't change what the bond is. The issuer still borrows. The coupon still pays. The maturity date still arrives.

What changes is how the bond is accessed, settled, and composed.

Traditional bond markets aren’t easily accessible. Many issuances require minimum purchases in the tens of thousands of dollars, and settlement times take one to two business days. This drives retail investors to typically access bonds through funds rather than owning them outright.

Tokenization lowers the barrier to entry, particularly for corporate bonds. Compressing settlement times to minutes is one benefit. The composability afforded by tokenization also allows bonds to integrate directly with DeFi protocols as collateral or yield-generating components.

But perhaps most importantly, the enhancements to due diligence processes facilitated by bond tokenization. Any attestations regarding the instrument or issuer can be easily associated with the issuance onchain, ensuring a tamper-proof digital paper trail remains in place. This registry significantly enhances auditability and enables investors to make more insightful comparisons across bonds.

The institutional adoption is already well past the experimental stage. BlackRock's BUIDL fund has grown to over $18 billion in assets across nine blockchain networks and recently became the first major institutional fund to trade on Uniswap. Franklin Templeton has prepared multiple institutional money market funds for blockchain-based distribution, including stablecoin reserve eligibility. The broader tokenized US Treasury market reached roughly $12 billion as of March 2026, up from under $1 billion two years earlier. The traditional US money market fund industry manages over $6 trillion. Even modest further institutional adoption implies significant growth.

The underlying asset hasn't changed. The access layer has.

Where Bonds Fit in the RWA Landscape

Bonds represent one of the clearest points of continuity between traditional and onchain finance. They're already trusted and understood globally. They already power everything from sovereign debt markets to corporate financing. What they haven't had is a distribution model that allows someone with a few hundred dollars and a crypto wallet to participate directly.

For onchain portfolios, tokenized bonds offer predictable, contractual income that integrates with the broader DeFi ecosystem. Where private credit derives yield from direct lending and payment financing derives yield from short-duration receivables, bonds derive yield from the sovereign and corporate credit markets. These are the deepest, most liquid capital pools on the planet.

The concept of a bond hasn't needed to change. It's the infrastructure that's finally caught up.

This material is for general informational and educational purposes only and does not constitute financial, investment, legal or tax advice. Tokenized assets involve risk and may not be suitable for all participants. Returns, performance and characteristics of traditional financial instruments may not translate identically to their tokenized counterparts. Always conduct your own research and consult qualified professionals before making decisions involving real-world assets or blockchain-based systems.