Real-World Assets are becoming a lasting part of onchain finance. At Plume we want everyone to understand this new ecosystem, built with traditional assets. The RWA Academy breaks down everything you need to know, from the most basic explanations to more detailed financial concepts. Here, we explain what treasuries and money market funds are as asset classes.

Sometimes boring is good. Especially in the cathedral of financial markets, where predictability translates to profit and architecture ranges from wildly complex to patently boring.

And perhaps the most boring corner of this cathedral serves as the cornerstone for the entire financial landscape. It’s not something that generates many headlines, and it doesn’t provide massive returns on investment. But it does protect capital while generating an unfailing stream of steady yield.

That unassuming and otherwise boring corner is treasuries and money market funds. And right now, it's become anything but boring. These reliable financial instruments are at the center of some of the most significant activity in onchain finance to date.

What Are Treasuries?

Governments, like all entities, need capital to survive. To get that capital, it borrows from investors by issuing debt. In the United States, that debt is issued by the Department of the Treasury and comes in different forms depending on how long the government needs to borrow for.

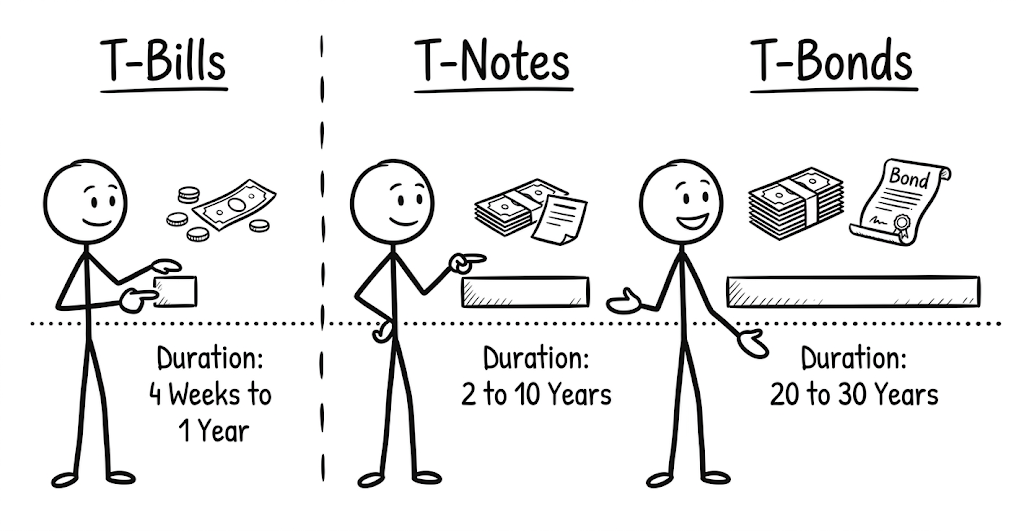

The shortest instruments, Treasury bills, mature in a year or less. Rather than paying periodic interest, they're sold at a discount to face value and redeemed at full value at maturity. The return is the difference between what you paid and what you receive back. Treasury notes extend from two to ten years and pay a fixed coupon every six months. Treasury bonds go out to twenty or thirty years and offer higher yields to compensate for the longer commitment.

US Treasuries are unique in one sense because they are backed by the full faith and credit of the United States government. This backing means Treasuries are considered the closest thing to a risk-free asset in global finance.

Businesses shutter and markets sputter, but Uncle Sam will continue paying his tab, or so goes the belief. It’s not a poorly founded belief either.

The Treasury market trades roughly $900 billion in volume every day, making it the deepest and most liquid securities market on Earth. Other governments issue their own sovereign debt on the same basic logic, with the creditworthiness of the issuing country driving the risk profile.

What Are Money Market Funds?

A money market fund is a pooled investment vehicle. It holds short-term, high-quality debt instruments like T-bills, along with high-grade commercial paper and repurchase agreements.

Investors deposit cash, and the fund then deploys it into a diversified basket of short-duration, liquid instruments. The yield flows back to investors, all while the net asset value stays stable at $1.00 per share.

Money market funds aren't savings accounts, and they aren't FDIC-insured. But for institutional and retail investors alike, they've functioned for decades as the practical equivalent: a place where idle capital earns a return without meaningful risk to principal.

The US money market fund industry manages over $6 trillion in assets. That figure alone says everything about how embedded this structure is in the global financial system. The relationship to treasuries is direct. When the Federal Reserve raises interest rates, T-bill yields rise. Money market funds then pass the higher yields of those T-bills on to investors. That's why money market fund yields moved from nearly 0% in early 2022 to above 5% between by the end of 2023. During this period, the Fed tightened aggressively, highlighting the deep links between the two instruments.

Why Do Investors Allocate Here?

Investors allocate to money market funds for different reasons than they allocate to long-duration bonds or riskier credit.

Treasuries and money market funds are not primarily return vehicles. They're stability vehicles. Institutions use them to park capital between longer-term investments, maintain liquidity buffers, and ensure that a portion of the portfolio is always accessible without a meaningful loss of principal. For a pension fund or endowment managing money on behalf of beneficiaries, that kind of reliability isn't a nice-to-have. It's a fiduciary requirement.

The other reason is duration risk, and this is where many investors get tripped up. Because T-bills mature quickly, they carry almost no sensitivity to interest rate moves. A 30-year Treasury bond can lose 20% of its value when rates rise sharply, as happened in 2022. A 4-week T-bill is largely indifferent to those same moves. You get yield without taking on the volatility that comes with extended time horizons.

Underlying all of this is something more foundational. The yield on short-term Treasuries is called the risk-free rate, and it serves as the benchmark against which all other investments are measured. If a riskier asset can't beat the T-bill rate, the extra risk isn't being compensated. Treasuries set the floor for rational allocation across all of finance, which is why every serious financial system in the world is built on top of them.

Why Bring Treasuries Onchain?

The case here is more straightforward than for almost any other asset class. T-bills and money market funds are already short-duration, highly liquid, and designed for access and stability. Tokenization doesn't need to reinvent the asset. It needs to fix the distribution.

And the distribution problem is real.

A retail investor trying to hold T-bills directly must first open a TreasuryDirect account, navigate a government portal that feels like it was designed in the Dot Com era, and then deal with purchase minimums and redemption timelines that don't match the pace of modern portfolio management. Money market funds are more accessible, but they still live inside traditional brokerage accounts, which can't interact with DeFi protocols, can't be used as onchain collateral, and don't settle on a blockchain.

Tokenized treasuries solve this by translating the risk-free rate's yield into an onchain-native format.

The preliminary numbers are compelling. BlackRock's BUIDL fund gathered over $500 million within weeks of launching on Ethereum. Franklin Templeton's tokenized money market fund reached $400 million at a similar pace. Ondo Finance's tokenized US Treasury product has seen sustained inflows from DeFi users seeking stable, yield-bearing collateral. In early 2026, the tokenized treasury market as a whole crossed $7 billion.

These aren't experiments. They're institutions moving real capital onto onchain rails because the infrastructure advantages are genuine.

When a tokenized T-bill exists onchain, it can serve as collateral in lending protocols, be embedded in structured products, and compose with other RWA instruments in ways that a traditional money market fund sitting in a brokerage account simply cannot. The yield is the same. The utility is fundamentally different.

Where Treasuries and Money Market Funds Fit in the RWA Landscape

Of everything being brought onchain, short-duration government debt has the clearest product-market fit.

It's the asset that institutions trust most, and it generates real, sustainable yield without leverage or credit risk. All without exposure to market sentiment. To top it off, it gives DeFi users it gives DeFi users a place to hold value that isn't correlated to crypto market cycles.

For onchain portfolios, tokenized treasuries, and money market funds, the foundation is laid. They're not designed to outperform. They're designed to provide stability, liquidity, and a dependable baseline return that makes the rest of the portfolio possible.

Every serious financial system in the world is built on top of a risk-free rate. The onchain financial system is building its version of that foundation right now.

The asset isn't new, but the infrastructure is finally being modernized.

This material is for general informational and educational purposes only and does not constitute financial, investment, legal or tax advice. Tokenized assets involve risk and may not be suitable for all participants. Returns, performance and characteristics of traditional financial instruments may not translate identically to their tokenized counterparts. Always conduct your own research and consult qualified professionals before making decisions involving real-world assets or blockchain-based systems.