.png)

Real-World Assets are becoming a lasting part of onchain finance. At Plume we want everyone to understand this new ecosystem, built with traditional assets. The RWA Academy breaks down everything you need to know, from the most basic explanations to more detailed financial concepts. Here, we explain what commodities are as an asset class.

Commodities are the raw, physical inputs the global economy depends on to function. While everyone interacts with them every day, filling up a gas tank, eating breakfast, or turning on a light, most people never think of themselves as participants in the commodity market.

But starting the car is quite different from turning a wrench under the hood. And as commodities move onchain, understanding what they actually are, why investors hold them, and what makes them structurally unique matters more than ever.

Before we talk about tokenization, we need to understand the asset itself.

What Are Commodities?

Commodities are raw materials used as inputs across virtually every industry. Unlike equities or bonds, they aren't financial constructs. They are physical things: oil, gold, wheat, natural gas, copper, uranium.

Their value is rooted in physical supply and demand. Not a company's earnings. Not a government's creditworthiness.

What makes commodities unique is that they are inherently fungible. One barrel of West Texas Intermediate crude is interchangeable with any other barrel of the same grade. One troy ounce of gold is recognized the world over. This fungibility is what makes global commodity markets possible, allowing standardized contracts to be written, traded, and settled at enormous scale.

Commodity markets are among the oldest financial markets in the world. Over centuries, farmers and merchants have managed uncertainty in raw materials markets through careful refinement of financial instruments. While the infrastructure of these markets has evolved dramatically, the underlying logic is the same.

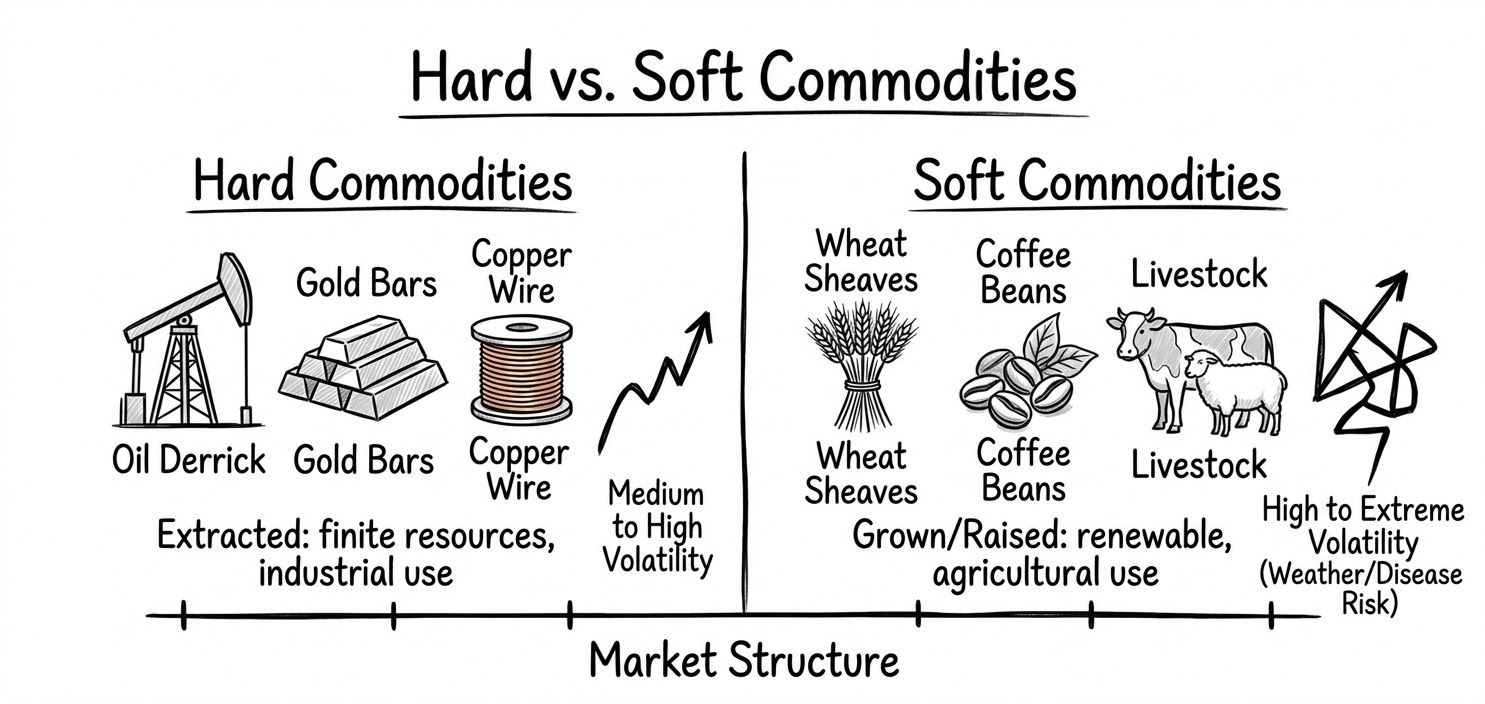

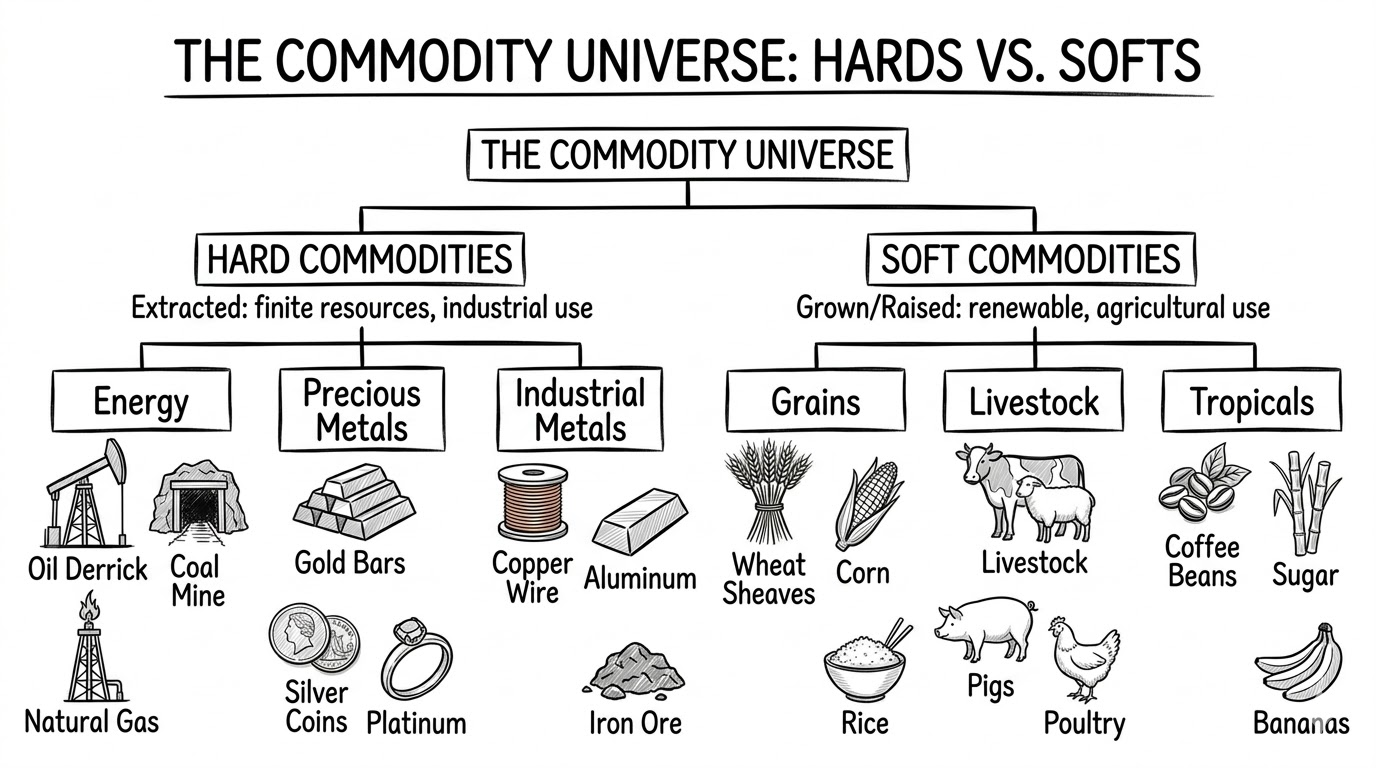

The commodity universe divides into two categories.

Hard commodities are extracted from the earth and require huge labor inputs to acquire. Think oil, gold, copper, and aluminum. All these are considered hard commodities.

Soft commodities are either grown or raised. Livestock and the grains grown to feed them, as well as tropical goods like coffee and sugar, comprise the soft commodities market.

These categories behave very differently from each other. A gold allocation moves on monetary policy and geopolitical risk. A copper allocation moves on manufacturing output and construction. A wheat allocation moves on weather, crop yields, and food security policy.

"Commodities" covers a family of asset classes as much as it does a single one.

Why Do Investors Allocate to Commodities?

Investors have many reasons to turn to commodities, but portfolio diversification, inflation protection, and their tangible value are the leading drivers for investment.

Diversification. Commodities have historically low correlations with other investment classes, such as equities and fixed income. While sentiment drives the stock market, commodity prices are primarily influenced by physical supply, weather patterns, industrial demand cycles, and other fundamental drivers. The 2022 inflation surge is a great example. As the S&P 500 fell 18% and bonds cratered 13%, the Bloomberg Commodity Index returned a tidy 17.5%.

Inflation protection. Commodities are one of the rare asset classes that moves in tandem with inflation. The rising price of goods and services is generally reflective of rising commodity prices. Research from Vanguard puts the inflation sensitivity of a broad commodity index at roughly 8x unexpected inflation, with no other major asset class coming close.

Tangible value. Regardless of what equity markets are doing, a physical tonne of copper is still a tonne of copper. It can still be drawn into wire, pressed into pipes, and assembled into electronics. That physical continuity, the fact that the asset's utility exists independent of any financial system, is part of why commodities have served as stores of value across centuries. A company's balance sheet cannot replicate that.

Commodities also move in extended multi-year periods called supercycles. During this period, rising prices are driven by structural demand growth, followed by a gradual decline as supply adjusts.

Commodities Are Diverse

Despite sharing a label, commodities are not a single risk exposure.

Gold is in a category all its own. With a market cap of over $35 trillion, it is one of the largest single asset classes on Earth, with central banks having purchased more than 1,000 tonnes of gold annually for three consecutive years.

Copper tells a different story. It’s an asset with a historical sensitivity to economic growth that’s currently being amplified by the global energy transition. Electric vehicles, solar panels, and other green technology requires a significant amount of copper. Analysts like Wood Mackenzie project EV-related copper demand to nearly triple by 2035.

Uranium is an incredibly unique commodity with a crucial role in global energy. Despite its highly controlled and regulated status, there is no formal exchange for uranium. Prices are published by just two private consultancies based on reported market activity rather than a public order book. The EIA found that 91% of uranium was delivered under long-term contracts in 2024, with only 9% trading on the spot market.

The varying levels of liquidity, accessibility, and market maturity among commodities highlight the asset classes’ inherent diversity.

Why Bring Commodities Onchain?

The physical nature that makes commodities valuable also creates real and persistent problems.

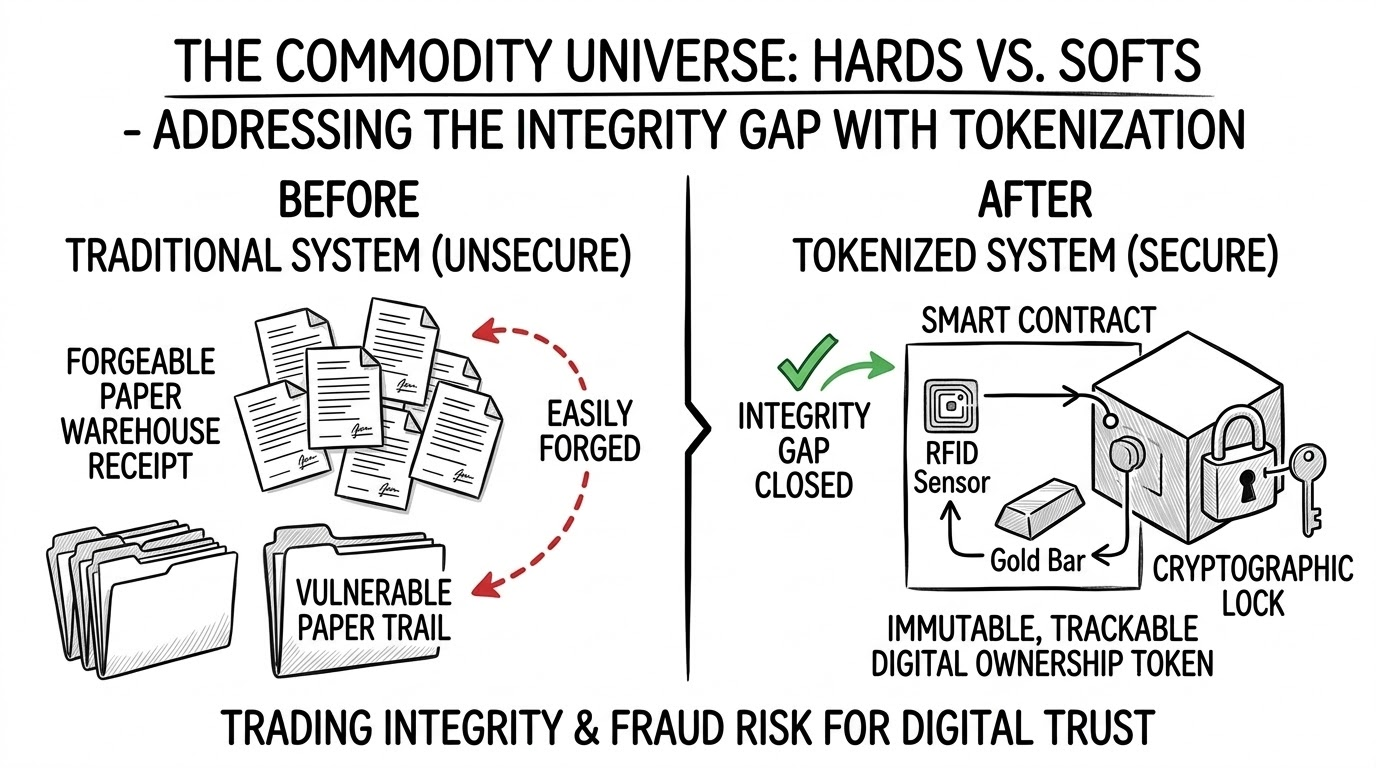

Commodity fraud is not a marginal issue. Because one tonne of copper is assumed identical to any other, ownership and quality are proven through paper documents rather than physical inspection of specific units. That trust gap has been exploited repeatedly and at enormous scale.

In 2014, a Chinese trading company pledged the same warehoused metals as collateral to multiple banks simultaneously, generating roughly $2.3 billion in fraudulent financing before the scheme collapsed. In 2020, a Chinese jeweler borrowed $2.8 billion from over a dozen financial institutions using gilded copper bars certified as genuine gold. In both cases, the fraud was only discovered accidentally.

The paper-based systems underpinning physical commodity finance had no mechanism to prevent it.

Tokenization changes this at the structural level. When a commodity is brought onchain, attestations covering quality, quantity, and custody can be encoded directly into the asset's smart contract. That record is tamper-resistant. When paired with physical validation technology like RFID tagging and third-party audits, the link between the physical commodity and its digital representation becomes far more robust than any paper document.

Price discovery is the other major benefit. CME gold futures go dark from Friday evening through Sunday. During those 25 hours, tokenized gold, specifically Tether Gold (XAUT) and PAX Gold (PAXG), become the only continuously traded, publicly visible gold instruments on Earth. According to Iggy Ioppe, former Chief Investment Officer at Credit Suisse, onchain markets are now responsible for virtually 100% of publicly visible weekend price formation for gold. When the CME reopens on Sunday evening, it reflects what happened onchain.

For a commodity like uranium, where the spot price is published weekly by a private firm based on voluntary reporting, continuous onchain markets could introduce something that doesn't currently exist.

A real-time price signal.

Where Commodities Fit in the RWA Landscape

Commodities are the oldest asset class in the world. Long before equities, before bonds, before any modern financial construct, humans were trading grain, metals, and livestock, and building financial instruments around them to manage risk.

Physical inputs to economic activity will always have value. They don't depend on a company continuing to operate or a government honoring its obligations. They exist in the world.

In the context of an onchain portfolio, commodities offer something distinct from yield-bearing assets like private credit or treasuries, and something distinct from growth-oriented assets like public equities. They provide tangible, real-world exposure that has historically moved with inflation, acted as a diversifier in stressed markets, and grounded a portfolio in the physical economy.

The gap between a commodity's physical reality and its financial representation has always been one of the asset class's persistent weaknesses. Onchain infrastructure has the potential to close it.

The physical commodity remains the same. How it is priced, tracked, and accessed is what evolves.

This material is for general informational and educational purposes only and does not constitute financial, investment, legal or tax advice. Tokenized assets involve risk and may not be suitable for all participants. Returns, performance and characteristics of traditional financial instruments may not translate identically to their tokenized counterparts. Always conduct your own research and consult qualified professionals before making decisions involving real-world assets or blockchain-based systems.