Real-World Assets are becoming a lasting part of onchain finance. At Plume we want everyone to understand this new ecosystem, built with traditional assets. The RWA Academy breaks down everything you need to know, from the most basic explanations to more detailed financial concepts. Here, we explain what payment financing is as an asset class.

Most people don't think twice about paying in installments. You buy something today and pay it off over time. Life goes on.

But behind that simple action sits a financial system that quietly and predictably moves nearly $4.2 trillion every year at scale.

Most people never interact with this system directly, but understanding it matters. Because for the first time, this kind of yield is becoming accessible beyond banks and institutions.

What is Payment Financing?

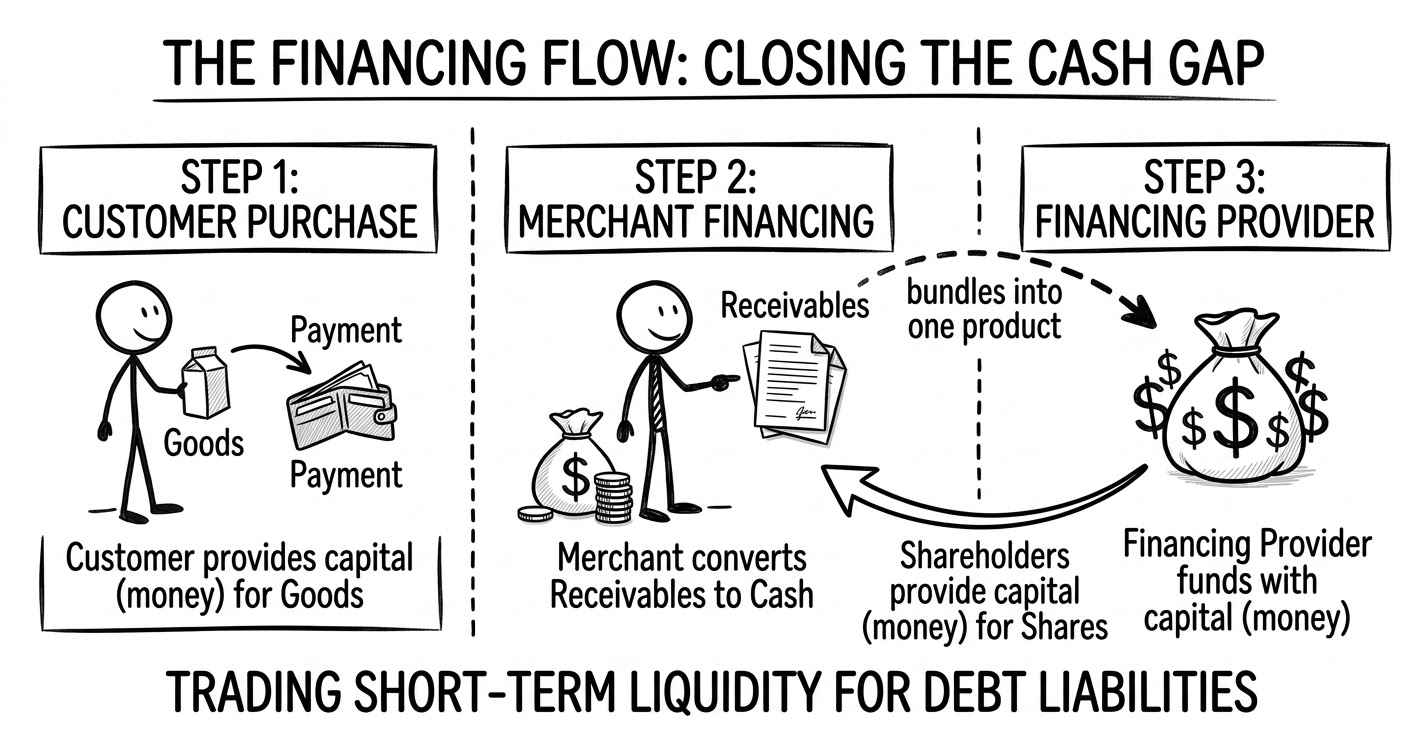

When you go to a store and choose to pay in installments, the merchant doesn't get paid instantly. You walk out with the product, but the merchant has to wait weeks or months to receive the full payment.

That waiting money already exists. It's legally owed, and it's scheduled. It just isn't in the merchant's account yet.

That future payment is called a receivable.

Payment financing is simply the act of turning those future payments into cash today. A financing provider steps in, purchases the receivable from the merchant at a small discount, and waits for the payment to settle. The merchant gets liquidity now. The financing provider earns the difference when the payment arrives.

You're not lending money for future spending. You're financing transactions that have already happened.

That distinction matters.

Here's the basic loop:

- A customer makes a purchase, already authorized

- The merchant wants cash now, not later

- A financing provider buys the future payment at a small discount

- The payment settles over time through card networks

- The difference between the purchase price and the settled amount becomes the return

Where Does the Yield Come From?

Yield exists in payment financing because merchants genuinely value immediate liquidity.

Waiting weeks or months to receive payment ties up working capital needed for inventory, payroll, rent, and growth. Many merchants would rather receive slightly less today than wait for the full amount later. That willingness to accept a discount is what creates the return for the financing provider.

This is sometimes called factoring, and it's one of the oldest forms of commercial finance in existence. The Babylonians practiced it. Medieval Italian merchant houses refined it. By the time the modern factoring industry took shape in the twentieth century, it had already been serving commerce for millennia.

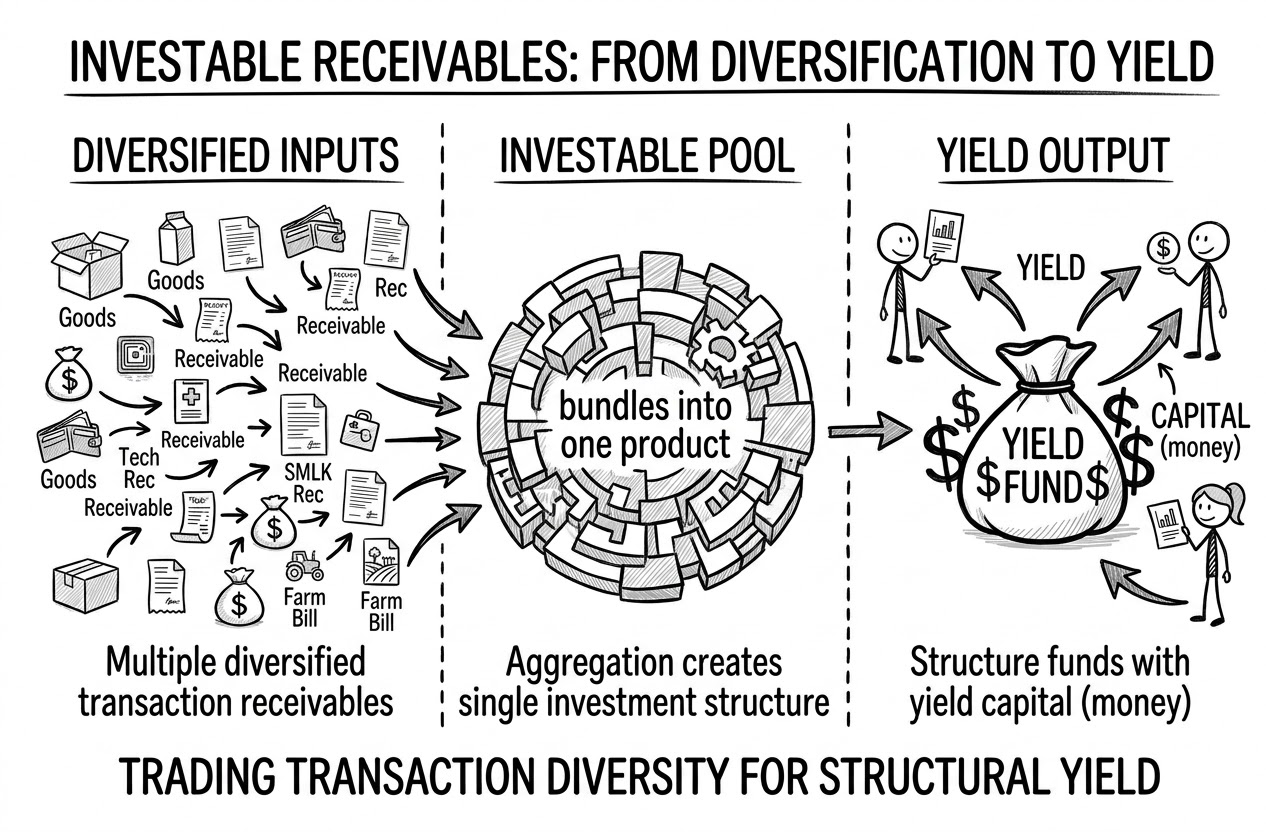

What makes payment financing particularly attractive as an asset class is how its structure manages risk. Because these transactions have already occurred, the underlying cash flow isn't speculative. The money is owed. The question is only timing, not whether it will arrive. Short settlement timelines, typically 30 to 90 days, mean capital recycles quickly. And because portfolios consist of thousands of small individual transactions rather than a handful of large exposures, the performance of any single receivable barely registers against the whole.

That granularity is the point. A global factoring network tracking over 4,400 companies across 90 countries reports credit loss rates below 0.04%. For context, investment-grade corporate bonds lose multiples of that over a five-year period. The asset class is not risk-free, but the structural diversification built into well-run payment financing programs is genuinely meaningful.

In traditional finance, payment financing already operates at enormous scale through banks, private credit funds, and asset-backed securities markets. The innovation isn't the asset class. It's who gets to participate in it.

The Mechanics Behind the Return

It helps to understand what you're actually buying when you invest in payment financing.

When a merchant sells a receivable, they typically receive 80 to 90 cents on the dollar as an upfront payment. The financing provider earns the remaining spread when the payment settles. Because these transactions are short in duration, the capital can be recycled many times over the course of a year, with each cycle generating its own return.

The risk profile is also structurally different from most forms of credit. A financing provider isn't underwriting a borrower's ability to repay a loan over three years. They're purchasing a payment that a customer has already authorized, with the card network or issuing bank effectively serving as the debtor. That's a categorically different counterparty than an individual SME borrower.

This doesn't make the asset risk-free. Defaults happen. Concentration in a single market or merchant type introduces its own exposure. And jurisdictional differences in consumer credit behavior can affect performance. But the asset class has proven itself through stress. Global factoring volumes dipped just 6.5% in 2020 before recovering with double-digit growth in 2021 and 2022. The short duration proved decisive: existing exposures ran off within weeks, and new originations could be immediately tightened. That's an advantage that longer-duration credit doesn't have.

Payment Financing Onchain

Payment financing has always had a transparency problem. In traditional markets, there's no reliable way to verify that a receivable actually exists, or that it hasn't been sold to multiple lenders simultaneously. The Greensill Capital collapse in 2021, in which a $3.5 billion supply chain finance firm imploded after lending against invoices that couldn't be verified, illustrated exactly what opacity looks like at scale. $10 billion in investor funds were frozen.

Blockchain doesn't just modernize access to payment financing. It addresses the specific structural weakness that has made the asset class vulnerable to fraud.

When receivables are tokenized, each invoice carries a unique, immutable reference on-chain. Double-financing becomes structurally impossible. Ownership transfers are transparent and auditable. Smart contracts can automate origination, verification, and settlement, and yield distribution, all without the intermediary layers that add cost and introduce opacity.

Stablecoins close the final gap. Cross-border payment flows that once took two to five days through correspondent banking now settle in minutes via USDC. That speed matters when the underlying receivable might mature in 30 days, as you can't afford a five-day settlement window eating into a month-long return profile.

The result is an asset class that has historically generated institutional-grade, short-duration yield, now accessible to a global investor base through onchain infrastructure. The same cash flows that have existed for centuries, moving through rails that are finally built for the twenty-first century.

Where Payment Financing Fits in the RWA Landscape

Payment financing is one of the most intuitive real-world asset classes to bring onchain, because its mechanics are already familiar to almost everyone.

Most people have paid in installments. Most people have used a credit card. The underlying cash flows are generated by the same everyday commerce that powers the broader economy. In Brazil alone, around 60% of all credit card transactions are paid in installments, with credit card financing balances surpassing a new all-time high of R$611 billion at the end of 2024. That's one country. The global picture is far larger.

What changes onchain is access. The same cash flows that have historically been packaged into opaque institutional vehicles can now be represented in a format that is observable, programmable, and composable within DeFi infrastructure.

For onchain portfolios seeking yield that is grounded in real economic activity, short in duration, and structurally diversified, payment financing offers a building block that most traditional investors never had access to in this form.

Same cash flows. Same commerce. Better infrastructure. Better access.

This material is for general informational and educational purposes only and does not constitute financial, investment, legal or tax advice. Tokenized assets involve risk and may not be suitable for all participants. Returns, performance and characteristics of traditional financial instruments may not translate identically to their tokenized counterparts. Always conduct your own research and consult qualified professionals before making decisions involving real-world assets or blockchain-based systems.