.png)

Real-World Assets are becoming a lasting part of onchain finance. At Plume we want everyone to understand this new ecosystem, built with traditional assets. The RWA Academy breaks down everything you need to know, from the most basic explanations to more detailed financial concepts. Here, we explain what public equities are as an asset class.

Public equities are among the most liquid and established asset classes in the world. Most people have heard of the stock market and have participated in it, whether directly through investment or indirectly through a retirement account.

But familiarity isn’t the same as understanding, and understanding what you own matters, especially as equities continue to move onchain.

Before we talk about tokenization, we need to understand the asset itself.

What Are Public Equities?

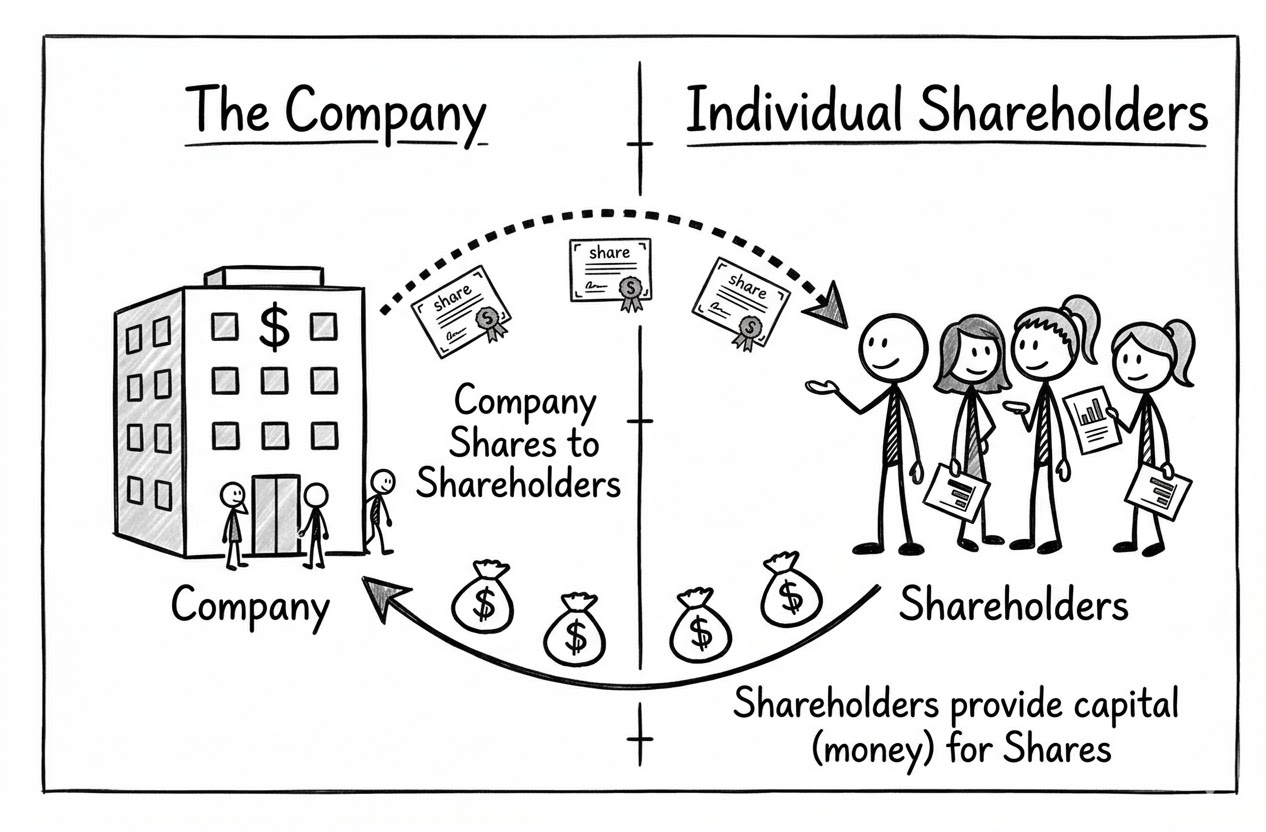

Public equities are shares issued by companies that trade on regulated stock exchanges. These regulated exchanges provide access to global investors, with nearly every major economy having at least one (often multiple) stock exchanges.

When you buy a share of a company, you are purchasing partial ownership in that business. This ownership gives you a claim on the company's future earnings and assets. The proportional number of shares you own is often the main consideration, but there are also different types of shares.

Some shares, such as preferred shares, come with voting rights. Other types of shares receive dividends when the company distributes profits. Understanding the rights and benefits that come with owning certain types and amounts of public equity shares is essential for maximizing your value.

Private credit refers to direct lending provided by private funds, asset managers, or specialized lenders outside the traditional banking system. A lender provides capital. A company agrees to repay that capital, plus interest, over a defined period. In theory, a simpler and more flexible process for borrowing money.

Over the past decade, private credit has grown into a major segment of global capital markets. It offers borrowers speed and flexibility.

For investors, it provides access to structured income tied to real operating businesses. In an investment class of its own, private credit gives investors the option to invest in a categorically safer, more predictable security (credit) - similar to high-yield bonds - rather than equity.

The word "public" is important here. It means the company has gone through the formal process of listing its shares on a public venue such as the New York Stock Exchange or NASDAQ. To be listed, a company must undertake significant disclosure, auditing, and regulatory compliance steps that don’t apply to private companies.

As a result, public equities are among the most liquid and transparent investments available. The market consistently sets the price of public equities during trading hours. This consistency means that average investors can generally buy and sell without issue during these predetermined hours.

The level of transparency, access, and liquidity sets public equities apart from their private counterpart. Private equity involves ownership stakes in companies that are not listed on any exchange, and these investments carry elevated risk. They are often less liquid, require significant minimum commitments and accredited investor status, less accessible, and do not carry the same reporting requirements and standards as public companies. Because of these limitations, public equities remain the de facto way for investors to get exposure to successful companies.

Why Do Investors Allocate to Public Equities?

Investors may allocate to public equities for several reasons. However, the most common among these are often growth, income, and liquidity.

Long-term growth. While the overall stock market tends to increase over time, the individual stocks that comprise it can fluctuate significantly. For example, despite significant crashes in 1987, 2001, and 2008, the S&P averaged 10% annual returns between 1928 and 2017. Historically, the long-term trajectory of broad equity markets has offered compounding growth that matches the broader economy.

Income. Some companies choose to distribute a portion of their profits as dividends in the form of regular cash payments. These payments are income in addition to any price appreciation, making them uniquely attractive to investors seeking income. Most dividend-paying stocks come from companies with stable cash flows in mature industries.

Liquidity. The ability to easily and quickly sell a stock during market hours is attractive to most investors. This flexibility gives public equities an advantage over other asset classes, such as real estate or private credit, where exiting a position can take months or be exercised only in specific redemption windows, subject to broader fund availability.

These characteristics have resulted in public equities comprising a core part of the average traditional portfolio. Easy to access, easy to understand, easy to sell.

Equity is Diverse

Perhaps what makes public equity the most interesting is that, despite these attractive qualities, public equity is not a single thing.

Rather, it is a broad category that encompasses thousands of companies across dozens of industries, each with very different risk and return profiles. Understanding the distinctions within public equity helps to explain how investors use it and, most importantly, what they’re actually buying.

Large Cap, Mid Cap, and Small Cap

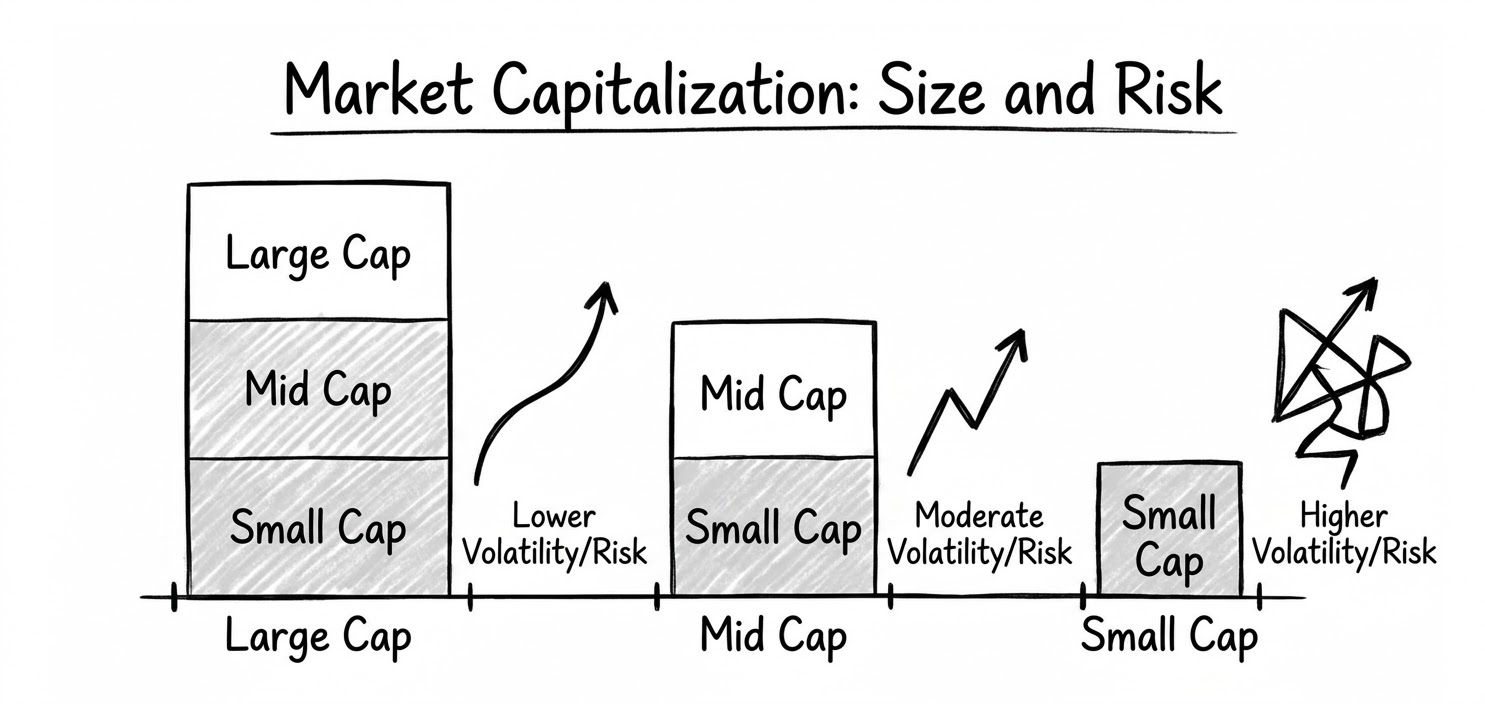

Companies are often grouped by their market capitalization, or market cap. This measurement is simply the total market value of all the outstanding shares for a given company.

Large-cap companies, with market caps above $10 billion, are the household names. Companies like Apple, Microsoft, and JPMorgan make up this category. These companies are well established, widely covered by analysts, and usually experience less volatility than their smaller counterparts.

Mid-cap companies, with between $2 billion and $10 billion in revenue, are generally established enough to have a track record. However, they still carry a growth potential and risk level that sets them apart from their large-cap counterparts.

Small-cap companies, usually valued below $2 billion, are still in their comparatively early stages of development. These companies can offer significant upside, but also come with more risk and price volatility.

All of this matters because a large-cap index fund and a small-cap growth fund are categorically different risk propositions. Even though they’re both technically public equities, they have less in common than one might assume at first glance.

Indices and ETFs: How Most People Actually Access Equities

Most retail investors don’t buy individual stocks. Instead, they use indices and exchange-traded funds (ETFs) to get exposure to the market, whether directly or indirectly through pension or retirement accounts like a 401k. While they may appear similar at first glance, indices and ETFs are distinctly different from one another.

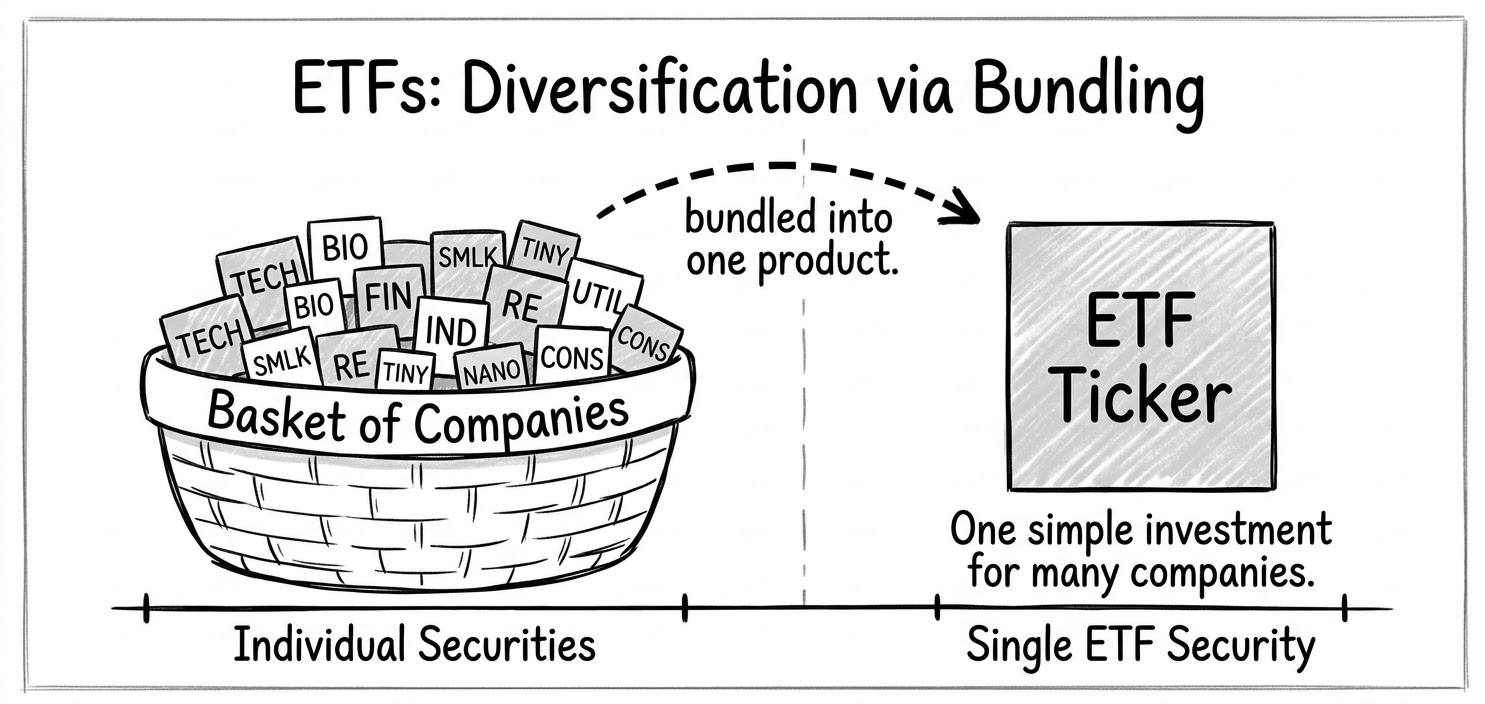

An index is a rules-based list of securities. It’s designed to represent and mirror a specific segment of the market. For example, the S&P 500 is an index of the 500 largest publicly traded companies in the United States, and the Russell 2000 tracks 2,000 smaller U.S. companies. These indices aren’t investments themselves. Rather, they benchmark the investment products they’re built around.

An ETF is a fund that holds a basket of assets. ETFs are often designed to track a specific index and can trade on an exchange like other equities. What distinguishes ETFs from indices is that, if you buy an S&P 500 ETF, you are buying a single instrument that gives you exposure to 500 companies simultaneously. The fund automatically rebalances as companies enter or exit the index.

ETFs changed how people invest in equities. They made diversification cheap and accessible. Before ETFs, building a diversified portfolio meant buying dozens or hundreds of individual stocks, which was time-consuming and expensive. Even more difficult for the average investor was rebalancing a portfolio over time to maintain adherence to diversification thresholds and preset strategies. Today, a single ETF can give a retail investor broad market exposure for a fraction of a percent in annual fees.

This matters for the RWA conversation because tokenized equities and tokenized ETF exposure follow the same logic. The goal is to extend that accessibility further, into onchain environments where new users live.

Why Bring Public Equities Onchain?

Tokenizing public equities means representing traditional shares as digital tokens onchain. The company and stock stay the same. The infrastructure is what evolves.

Traditional equity settlement takes two business days after a trade, a relic of an era when paperwork had to physically move between institutions. Tokenized equities can settle in seconds. That significant improvement reduces counterparty risk, frees up capital, and opens the door to 24/7 global markets.

Tokenization also enables more granular fractional ownership. A single share of a high-priced stock like Berkshire Hathaway Class A trades at hundreds of thousands of dollars. Tokenization makes it possible to own a fraction of that share without needing a specialized brokerage product to facilitate it.

There is also the composability angle. Onchain equities can integrate with DeFi protocols, be used as collateral, or be combined with other RWAs in ways that are simply not possible in traditional financial infrastructure. The asset remains regulated. The wrapper changes how it moves and what it can do.

Where Public Equities Fit in the RWA Landscape

Public equities bring growth-oriented, market-driven exposure into the RWA ecosystem.

Unlike income-focused assets such as private credit or treasuries, returns on these assets are shaped by company performance, innovation, and broader economic cycles. They are volatile by nature, marked-to-market every business day the stock market is open, and subject to swings in public sentiment. That volatility is the price of the upside, best calculated in long-term price changes rather than in APY (yield) figures more familiar to the earn category, where we find fixed-income instruments.

For onchain portfolios built primarily around yield-bearing RWAs, tokenized equities offer a different kind of building block. One that captures long-term growth rather than contractual income.

The market is large, deeply understood, and already accessed by hundreds of millions of people globally. Bringing it onchain does not require convincing anyone that equities are a legitimate asset class. It simply requires making them move better.

This material is for general informational and educational purposes only and does not constitute financial, investment, legal or tax advice. Tokenized assets involve risk and may not be suitable for all participants. Returns, performance and characteristics of traditional financial instruments may not translate identically to their tokenized counterparts. Always conduct your own research and consult qualified professionals before making decisions involving real-world assets or blockchain-based systems.